One goal of your stock ETF savings plan is likely retirement provision. Because with retirement comes the best part of decades of saving: you sell your ETF shares bit by bit and can enjoy the returns of the past decades. With a trick, you can potentially get significantly more out of it - if things go well, tens of thousands of euros more.

That is due to the tax rules for your depot. When you sell ETF shares, the principle of 'First in, first out' (FIFO) applies. The shares that entered the depot first will also be sold first.

The problem: With the old shares, you most likely made the biggest profits because you hold them the longest. And the higher the profits, the more taxes you have to pay when selling the shares.

Change ETF every 10 years and benefit

To prevent this, you use the Finanztip 3x10 strategy. This way, you can decide for yourself which ETF shares to sell first by not only investing your money in one stock ETF, but regularly investing in a new one every ten years - at least three times. Because 30 years is a typical period for long-term investing in an ETF.

The new ETF can track the same index as the old one – so you can, for example, invest in three different stock ETFs on the MSCI World. During the withdrawal phase, you can then reverse the roles and sell the most recent ETF first – the one that has made the least return and therefore incurred the lowest taxes.

Plan for the savings phase

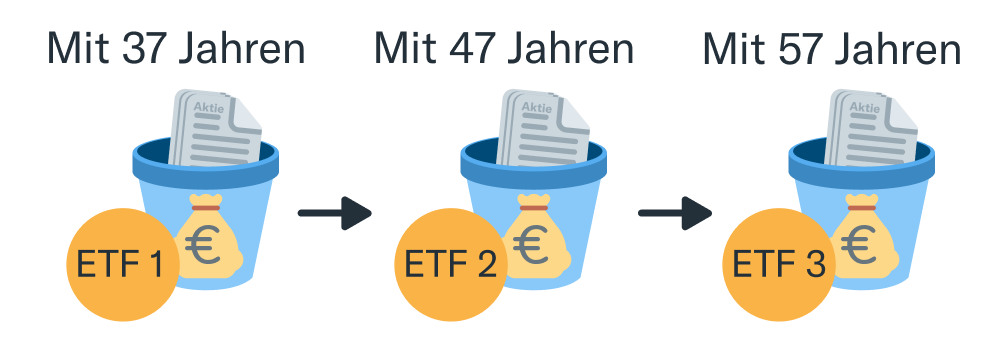

Let's go through the 3x10 strategy step by step with an example. Instead of always investing your money in the same ETF, you divide the investment over time into three different ETFs:

- ETF 1: You invest €36,000 once at age 37. This corresponds to €300/month over ten years (from 28 to 37)

- ETF 2: You invest €48,000 once at age 47. This corresponds to €400/month over ten years (from 38 to 47)

- ETF 3: You invest €60,000 once at age 57. This corresponds to €500/month over ten years (from 48 to 57)

If we add up all three ETFs, assuming a 7% return per annum, at the age of 67 you will have nearly €578,000 gross in the portfolio. However, the money is distributed quite differently: ETF 1 is worth €274,000, ETF 2 €186,000, and ETF 3 'only' €118,000.

Plan for the withdrawal phase

Now let's assume that you want to withdraw money from your ETF portfolio in three steps as you age. €180,000 at 67, €300,000 at 77, and €420,000 at 87 - all net, after taxes. You withdraw more each time because you have to factor in inflation and increasing care needs. The shares you do not sell (yet) continue to rise at 7% per annum in our example.

Sale of shares: Without 3×10 strategy

If you have only invested in a single ETF all your life, here comes the problem: When you click on 'sell' in your portfolio, you are selling the oldest shares first - those from the time when you were 37. These shares have accumulated much more profits over the years than the newer ones, and these profits are now taxed at 18% (30% are tax-free due to partial exemption, the remainder is subject to capital gains tax (25%) and solidarity surcharge).

In order to reach your desired withdrawal of 180,000€, you have to withdraw more money from the ETF due to higher taxes than you would with newer shares. However, you do not have this choice, so there will be less money left in the ETF that can continue to grow over the 20 years until the final withdrawal. After the last withdrawal of 87, you will be left with shares worth nearly 165,000€ in the depot, which you could inherit (or sell).

Sale of shares: With 3×10 strategy

If, on the other hand, you use the Finanztip 3×10 strategy and invest in three different stock ETFs every ten years, you can avoid the problem: Your portfolio will not only contain a single ETF position, but ETF 1 (used from 37 to 47), ETF 2 (used from 47 to 57), and ETF 3 (used from 57 to 67). Each of the three ETFs has its own identification number and can be sold separately by you.

For your first withdrawal of 180,000€ net, you first withdraw the complete 118,000€ from ETF 3 - the youngest of your three ETFs with the lowest gains and taxes - plus 84,000€ from ETF 2, the second youngest. With 77, you use up the rest of ETF 2 and touch ETF 1. With 87, you withdraw money from ETF 1. In the end, you don't have 165,000€ net left, but 193,000€ - so with the Finanztip 3x10 strategy, you end up with 28,000€ more.

So you implement 3x10 most easily

- If you are already investing in an ETF: Check when you bought the first units. If you have been investing in your ETF for five years, you can continue with this ETF for another five years before switching to ETF 2, and after ten more years to ETF 3. Have you been investing for twelve years? Then switch directly to a new ETF now and switch again in eight years.

- If you are not yet investing in an ETF: Once you start, the first ten years will be with ETF 1 - then you switch to ETF 2 and so on.

- So you find a new ETF every ten years: If you invest in the MSCI World, you can start with the 'Xtrackers MSCI World UCITS ETF' (WKN A1XB5U), then switch to the 'Amundi MSCI World UCITS ETF' (WKN A2H59Q), and finally to the 'Invesco MSCI World UCITS ETF' (WKN A0RGCS). The three ETFs are separate but extremely similar funds, as they all track the same stock index. You can find more suitable ETFs in the ETF-Finder by Finanztip.

- Write down in which period you invest in which ETF. If you invest for more than 30 years, you can even get more out of it and use a 4x10 or an 8x5 strategy instead of the 3x10 strategy, i.e., forming four or even eight different tranches. Then accounting becomes particularly important.

- You have already accumulated a lot of money in a single ETF? Even then, you can use the Finanztip 3x10 strategy. Find out how in the regular Finanztip newsletter on Friday.

- If the strategy sounds too complicated to you? Then continue to invest in a single ETF, as this way you still have good chances of a decent return in the long run. With the Finanztip 3x10 strategy, you can achieve even more with relatively little effort.

One pitfall remains: Our strategy is based on today's tax rules. These may change in the future. But at least you secure yourself a good chance of being able to claim significant tax savings later on.

You can find everything else about the 3x10 strategy in our new guide 'Selling ETFs'. Prefer to watch it as a video? Saidi reveals more details in the video linked on YouTube. Still have questions about the Finanztip 3x10 strategy? Then visit the Finanztip Forum and join the discussion!

Ed. note: Originally, the text stated that you would have to withdraw the entire €118,000 from ETF 1 and €62,000 from ETF 2 on the first withdrawal. In reality, you need to withdraw €118,000 from ETF 1 and €84,000 from ETF 2 to receive a net amount of €180,000. However, this does not change the end result; your advantage remains at €28,000. We have adjusted the corresponding section.

We want to help as many people as possible with our recommendations to manage their finances themselves. Therefore, our content is freely available on the internet. We finance our elaborate work with so-called affiliate links. We mark these links with an asterisk (*).

At Finanztip, we handle affiliate links differently than other websites. We only link to products that have been recommended by our independent team of experts. Only then can the respective provider have a link to this offer set. We receive money when you click on such a link or conclude a contract with the provider.

Whether and to what extent we are compensated by a provider has no influence on our recommendations. What our experts recommend to you depends solely on whether an offer is good for consumers.

More information about our working methods can be found on our About Us page.